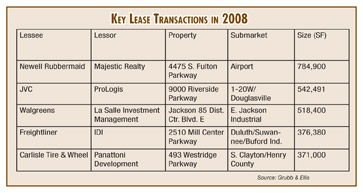

|

SOUTHEAST SNAPSHOT, FEBRUARY 2009

Atlanta Industrial Market

Atlanta’s industrial market has taken heavy blows from the recession. Before the market bottomed out, developers pushed through projects for industrial buildings leading to a current rash of overbuilding. This landscape of empty new developments has proved a burden for developers, but tenants are reveling in the amount of space available.

“Even if the economy turned around today, there are several years of supply currently in the market,” says Eric Weiss of Studley’s Atlanta office. “That being said, it’s a great time to be a tenant. Companies that need space right now are in a unique position to demand and receive numerous concessions from landlords such as reduced rental rates, free rent and most importantly, flexibility in lease terms including cancellation, contraction, expansion and renewal rights.”

In the fourth quarter of last year, Atlanta’s industrial woes came bubbling to the surface. Thirteen buildings totaling 1.3 million square feet were delivered to the market, causing a massive softening throughout the city. Weiss estimates that 80 percent of the city’s tenants lease space in chunks smaller than 50,000 square feet, so the prospect of filling more than 1 million square feet is daunting. “Most of the buildings that are vacant today will still be vacant in a year, and those that are filled will likely be cannibalizing tenants from other buildings,” Weiss says.

In a market that is decidedly pro-tenant, Kate Sharp of Atlanta-based Ackerman & Co. is still seeing her clients close down expansion plans. “Some tenants are holding tight, wanting to expand but waiting to see what’s going to happen,” she says. “Everybody’s just sitting tight and waiting to see what everybody else is going to do.” That goes for some developers, as well. Last year, AMB Properties completed a 109,845-square-foot warehouse, the first phase of a 327,000-square-foot project. Construction was supposed to commence on the second phase last fall, but that’s been put on hold due to economic worries.

Even in these overbuilt times, buildings that were in the works when the economy headed south are coming online. “There are buildings that are still under construction and will deliver that will only serve to help my clients leverage their position within the market,” says Weiss, who predicts a large amount of projects being scraped, further benefiting his tenants. A return to confidence is one thing that will help refuel the market, Sharp says. She thinks 2009 will be a major struggle for everyone involved in the industrial market, but that things will start turning around during the fourth quarter. “A lot of people in my generation haven’t seen this at all,” Sharp says. “Everybody’s just scared of 2009.”

— Jon Ross

Industrial Market Mirrors Activity in Atlanta’s Office Sector

Systemic overbuilding in the Atlanta industrial market can be compared to the current crisis in the office market. The lack of tenants in nearly-complete Buckhead and Midtown office buildings has been widely reported as a dire circumstance, but brokers say there is historical basis for these problems. “A lot of it comes back to bigger decisions made by the developer’s investment heads,” says David Zanaty, vice president of office at AIG in Atlanta. “In the most recent cycle, Class A office space in Atlanta was selling for upward of $400 per square foot — well over replacement costs. When you look at that, you say, well,

it makes more sense to build than it does to buy stabilized office space … It’s not irrational.”

This same attitude led developers to build large industrial buildings with little or no tenant base, trusting that interest would be generated once the properties reached completion. But now that all the industrial space has been delivered, the only thing to do is take a cue from the office market.

“That stuff is coming onto the market, and it’s going to drop effective rates,” Zanaty says. “People are just going to have to navigate it.” |

©2009 France Publications, Inc. Duplication

or reproduction of this article not permitted without authorization

from France Publications, Inc. For information on reprints

of this article contact Barbara

Sherer at (630) 554-6054.

|